John Kammerer, CPA

John Kammerer, CPA

Real-Life Lessons from Deal Leaders: How to Mitigate Risk in an M&A Transaction

Mergers and acquisitions create opportunity. They also introduce risk at every stage of the transaction lifecycle.

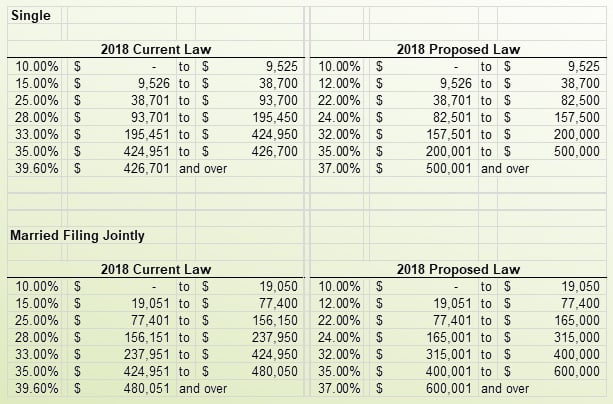

November 19, 2017 — On Friday, December 15, 2017, the Conference Committee released a reconciled version of the "Tax Cuts and Jobs Act". The House and Senate have since voted it into law.

Below is a summary of some of the major provisions of the bill.

Mergers and acquisitions create opportunity. They also introduce risk at every stage of the transaction lifecycle.

The Minnesota Paid Family Leave Act (PFLA) is already changing conversations inside leadership teams across the state. Most employers understand the...

If you’ve been through a 401(k) audit, you know the audit itself isn’t usually the issue. The real challenge is the disruption and last-minute...